Oil curve points to shock, not lasting disruption

By Fei Xu, Vanguard Commodity Strategy Fund Portfolio Manager

Markets and economy

Navigating volatility

Despite the shock, markets expect a quick fix, not a lasting supply loss

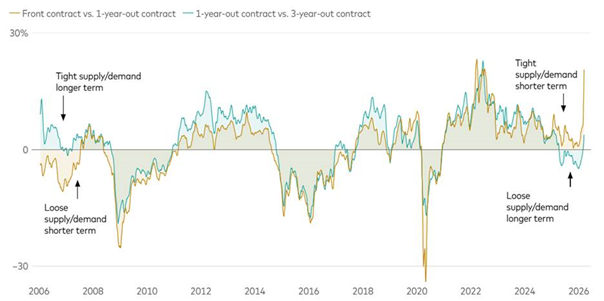

The outbreak of conflict in Iran has abruptly ended the unusual oil‑market dynamic. At that time, geopolitical risk premia supported the front end of the Brent curve even as weakening supply-demand fundamentals weighed on longer‑dated spreads. The conflict has brought those forces into sharper alignment.

Expectations for oil supply and demand converge anew

Note: Data reflect 30-day moving averages of Brent crude spreads.

Sources: Vanguard calculations, based on Bloomberg data, as of March 16, 2026.

It has also triggered one of the largest oil supply disruptions in decades, centered on the effective closure of the Strait of Hormuz. Roughly 20% of global seaborne oil trade—and a similar share of liquefied natural gas—flows through the strait, making the duration of disruption the key determinant of further energy price spikes. Near-term prices have spiked as supply has been curtailed.

Importantly, while short‑ and long‑dated Brent crude spreads—key indicators of supply-demand conditions and geopolitical risk premia—have moved into closer alignment since the start of the conflict, the response further out on the curve has been comparatively muted. The Brent 36‑month contract has risen only modestly since late February, compared with a much larger spike in the front-month contract. This divergence suggests that, despite the severity of the near‑term shock, market participants continue to expect a relatively swift resolution rather than a long-lasting loss of supply.

That said, $100‑plus Brent is no longer an extreme outcome: The front-month Brent contract traded over $100 from March 12 through March 17. A protracted period of oil over $100 would weigh on growth and spur inflation in the U.S., the euro area, and Japan.

The oil shock is now feeding directly into broader macro pricing through terms‑of‑trade‑driven currency moves, higher near-term interest rates, and suddenly rising inflation expectations. As elevated oil prices persist, concerns about economic growth and tightening financial conditions are complicating monetary policy outlooks.

As events continue to unfold, oil markets will remain a critical barometer of escalation risk. For investors, the message is unchanged: Periods of geopolitical stress can drive sharp, unsettling price moves, but discipline and a long‑term perspective remain essential amid heightened volatility.